The ancient fintech innovation which is still used today

The story is told again and again that in earlier times goldsmiths realized that only a fraction of the gold deposited with them was being called up and THAT'S WHY they started issuing gold certificates that were virtually covered by the gold lying around idle. It is simply assumed - as if this were self-evident - that the goldsmiths had misappropriated the gold entrusted to them, one could even say embezzled it. I consider this to be an untenable position, because such a crime was of course punishable in those days, and given the hair-raising prison conditions of the time, one can almost certainly assume that such embezzlement never took place.

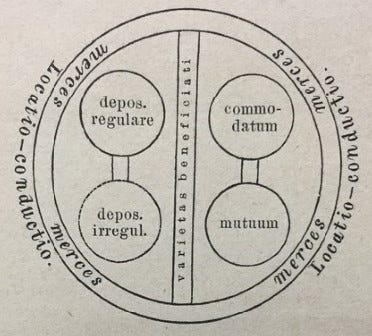

However, as soon as one differentiates this according to the type of safekeeping, new possibilities arise. As long as the safekeeping contract was structured as a depositum, the goldsmiths' hands were tied, as they were not allowed to dispose of the assets entrusted to them. This changed when the safekeeping agreement was structured as a commodatum or mutuum, where the custodian was allowed to use part of the assets for his own account (commodatum) or, finally, the assets handed over became the property of the custodian (mutuum) and only restitution of the same kind and quality was agreed. In addition, in the case of commodatum and mutuum, remuneration for the depositor could also be agreed, whereas in the case of deposita, the depositor usually had to pay a fee for the service of (safe) storage.

One can therefore argue about the sources from which the goldsmiths had acquired the necessary gold reserves. This is not so decisive, but it is important to realize that the development of "paper payments" was not initiated with embezzled funds, but with their own. The goldsmiths made use of an innovative financial construction that is largely unknown under the name of "credit lending". Two contracts were combined: a contract for the transfer of a claim/debt instrument, which was endorsable and functioned practically like a bill of exchange, and a payment agreement under which the customer had to make a payment to the goldsmith/bank at a future date. In detail, the deal worked like this: first, the goldsmiths or banks issued a bill of exchange, which they made out to themselves as the debtor. These are also sometimes referred to as promissory notes. Due to the ambiguous use of this term and to avoid the risk of misinterpretation, the term "Solabill" (from the term “Solawechsel”) is used here for this financial instrument. A Solabill is a securitized claim, even if it is issued by the debtor named in the bill. But beware, it is not a claim for the issuer, but for non-issuers it represents a claim against the issuer with the amount owed noted within.

The first contract (1) consisted of the delivery of a Solabill to a customer who could use it at will, in particular for transactions with sellers of goods or investment goods. If the bank was widely known to be solvent, this Solabill was readily accepted, especially as it could also be interest-bearing. The term ob these bills was usually 3 months, after which it had to be presented to the bank for payment. (If the deadline was missed, the debt was not forfeited, but the direct enforcement rights laid down in the Bills of Exchange Act were. Missing the deadline converted the securitized bill into a not-securitized claim.) The bank therefore had to pay the Solabill it had issued. This would be a bad deal if it were not for the second contract (2), which obliged the customer, who had received the Solabill first, to pay the amount of the bill to the bank one day before it was due (3). If the customer fulfilled his payment obligation (not securitized but usually collateralized), the bank was able to settle its debt from the presentation of the Solabill the next day (4), whereby the bill lost its validity and all transactions carried out with it were finalized. This arrangement is not a loan like today because the customer did not receive gold (i.e. the generally used means of payment), but, with the Solabill, a securitised claim paper against an institution known to be solvent, which could be used to settle transactions without the actual consideration in gold actually being paid. There is in a strict sense no “payment” possible with the paper, because the transfer of the Solabill is more a securitised form of a supplier´s credit, where the payment comes due through the final settlement of the Solabill (4). When the final payment of all transactions carried out with the Solabill was made on the due date, then all pending liabilities (which constitute something like a “credit chain”) were considered to have been settled in one fell swoop. This means that for a large number of transactions carried out with the Solabill as a payment promise, the required means of payment, gold, was only needed ONCE and therefore the (scarce) gold stock was "economized" to a certain extent with this fintech innovation.

As long as all parties involved fulfilled their obligations, a bank could not get into payment difficulties because it could always collect the gold required to pay the Solabills one day before maturity (3). If the current bill holder preferred to have liquidity instead of the bill, he could redeem it early at his bank or the debtor bank, which meant that the bank actually had to forego the amount of liquidity paid early until the Solabill matured. Insofar as the bills bore attractive interest rates, only a few of them in circulation were actually presented for early payment. This means that the bank/goldsmith only had to hold a fraction of the effective means of payment (the means of payment noted on the Solabill - Gold) for all the bills in circulation. And thus it becomes clear that, depending on how long the average holding period of these bills was, the bank/goldsmith had to have a high or low percentage of effective means of payment on hand. If business was good and confidence in the future was positive, only a few Solabill were redeemed; if the outlook was poor and liquidity pressure was high, a correspondingly large number of bills were submitted. This was not a problem as long as the payment contracts (2) with the Solabill customers were settled on time (3), because then it was merely a bridging problem. However, if the economic situation got into a crisis and the payments for the Solabills (3) could not be made, the bank/goldsmith had to make up for the submitted papers from its own gold stocks. It doesn't take much thought to understand that once a certain default rate is reached, the available liquidity reserves are no longer sufficient, which then (rumor has it) leads to all the bills in circulation being presented for payment and the bank/goldsmith having to file for bankruptcy. It would be too short-sighted to blame the amount of securitised claims issued or the issuers of these securities for this, because to date the reliability of forecasts with regard to crises that can and will occur is more than poor, just think of the "surprises" caused by the GFC. It is more of a kind of irrational exuberance during times, where expectations into the future are promising, which gives rise to these disastrous developments.

It has probably already been noticed that the phenomenon of "fractional reserve banking" arises almost automatically with this type of fintech, because in normal business conditions - normal being defined as a situation in which the loss write-offs due to defaulted bills can be covered by the interest income from the bills served - only a small proportion of the bills in circulation are discounted prematurely (before maturity) at the bank and, in addition, the default rate is so low that the bill business is worthwhile for the banks. In other words, as long as the majority of the bills of exchange (Solabills) are serviced on time, the liquidity costs for the banks remain very modest, which also underlines the bank's creditworthiness to the outside world. In extreme cases, if all Solabills are submitted on the due date and all bill payments are made on time by the customers, the bank has an effective liquidity requirement of 0, zero, nada gold units. The banks/goldsmiths in this case therefore had no need to grant “credit lending” with the depositors' gold holdings.

Now one may ask why such a construction was necessary. The answer is simply that the usual means of payment at the time, gold, would not have been sufficient for all business transactions, which was not only due to the growing economy, but also to the fact that the European continent had a permanent payment deficit with the Asian economic area, because European goods were not attractive there and therefore had to be paid for with precious metals. (It would appear that this relationship has now been restored). However, as the Europeans were very keen on porcelain, silk, tea and spices, there was a permanent outflow of gold and silver, which could not be covered by their own mines. The consequences are not difficult to understand: Precious metals became scarce in Europe because of Asian demand, so they became a sought-after commodity, which incidentally explains why the standard for payments in trade became a precious metal standard - the Asians got the Europeans into this. So it is not any "intrinsic values" that are supposed to be inherent in gold, or the difficulty of "divisibility" - scissors or a knife are not enough - or the durability that does not explain why gold coins have strangely always suffered from "abrasion", but the demand of Asian trading partners who did not want to be fobbed off with any glass beads. These were finally the reasons for the raids into Latin America and the opium wars.

It is important not to lose sight of the fact that, despite the Solabills in circulation, which were eventually called "banknotes", gold was ultimately the actual means of payment, while the bills/banknotes merely functioned as a substitute or deferred means of payment. They were not "another form" of gold, but elementary promises of payment in gold, which could either be claimed in cash, credited, or used for a transaction because the debtor was a known solvent actor - the similarities with the current payment system are in no way a coincidence. The central difference, however, is that today's cash bills (there are no longer banknotes, because banknotes have a claim content, cash bills do not) have taken over from gold as the ultimate means of payment, whereby they have one central characteristic in common with gold: like gold, they are neither a claim nor a liability. The transition took place rather abruptly with Nixon's declaration in 1971 that the USA was no longer solvent (it remained so) and therefore the possibility of redeeming paper dollars in gold at the fixed rate (which was only permitted for states anyway) would be "temporarily suspended".

To maintain the designation as “banknote” was probably due to the fact that the cash bills that followed the banknotes in 1971 looked very similar to banknotes and, in order to avoid panic and crises, it seemed necessary to leave everything as it was - including the designation as "banknotes". Of course, this was not entirely possible without coercion, so that the acceptance obligations, which were already legally binding beforehand, now took on even greater significance. Anyway.

It is important to note that today's payment system functions in exactly the same way as it did at the time of the gold standard. Even today, it is mainly the promises of payment (like the Solabills) that are responsible for the transfer of money at the central bank, with the main aim of paperless payment transactions being the suppression of legal tender. Even if cash is no longer scarce, as gold used to be, the financial sector earns its commissions more from credit and payment transactions, but less from legal tender. The fact that the fintech innovation of over 200 years ago still provides the template for the functioning of the financial system today should give rise to doubts as to whether today's "innovations" justify the trust placed in them.

Thanks for that detailed historical exposition, which puts some great color on my own "discovery" that the mechanics of "money creation, then and now" have not changed -- with the notable and obvious exception of the "standard money," which used to be gold but which is now paper, printed virtually at will by governments. It's hardly possible that bank credit creation would survive years of popularity in the marketplace if it were merely a scam. Good business ideas usually survive and thrive through the ages, and this basic banking technology, which benefits all parties to the transaction, is a good example. Scams cannot, by definition, be a "win-win."